I know where yams come from. I can name every country through which the Danube runs. I can even bake a quiche from scratch. But when it comes to monetary policy, financial indexation, so-called external shocks and wage formation, I feel like a beached whale. A rotting beached whale. Asking around for answers led to the realisation that the general population is equally informed about these subjects—which is to say not at all. We are a pod of putrid beached whales. This is dangerous in a country that has experienced one of the most severe economic collapses in modern history—a country where money and the economy sometimes feel like the only relevant topics of conversation.

I tried to address the issue by starting from a familiar, but too-often empty locale—my wallet. My question was simple: How come I have 3 grand in my pocket and still feel like a pauper?

“I’m Much Too Fast to Take that Test”

The simplest answer to that question is inflation, or the steady rise in the general price of goods and services and the subsequent erosion of a currency’s purchasing power. The general consensus between economists is that inflation is not altogether a negative phenomenon, but a natural by-product of the economy and dependent on wages, prices for goods and interest rates. Inflation has both pros (debt relief, the balancing of labour markets) and cons (purchasing power and investment uncertainty). Most countries aim for low inflation, somewhere in the 1%–3% range.

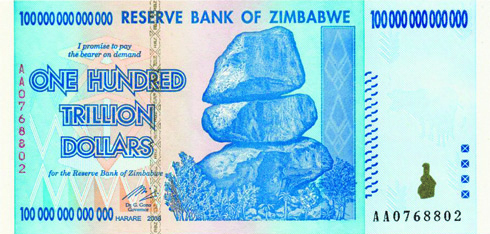

Extreme inflation, on the other hand—otherwise known as “hyperinflation”—tends to have catastrophic effects. Commonly defined as a cumulative inflation rate of 100% over three years, hyperinflation is characterized by a central bank printing successively greater denominations of currency, rendering previous bills worthless. The best example of hyperinflation might be Hungary during the summer of 1946, when the post-war government crumpled under an inflation rate of 41.900,000,000,000,000%—the highest ever recorded. The value of the Hungarian pengo doubled nearly every 13 hours and led to the printing of the largest banknote denomination ever issued: the 100 quintillion (100,000,000,000,000,000,000) pengo note.

While the Icelandic króna has never reached such eye-gouging extremes, the history of Iceland’s currency is volatile enough to lead a number of experts to question whether the country shouldn’t abandon it altogether.

“And My Time Was Running Wild”

Throughout the post-war period, Iceland’s inflation has been well above the average of other members OECD (the Organization for Economic Co-operation and Development, a collection of democratic, free-market economies). From 1945 to 1973, yearly inflation hovered in the moderate 10–15% range.

All that changed in the early 70s. With a population of just over 200.000 and an economy dependent on export trade, Iceland was particularly vulnerable to the oil crisis of 1973. Import prices grew and inflation followed fast on its tracks. A second oil shock in 1980 only exacerbated the situation. A fall in the fish catch of 1982 was the third wheel of an inflation tricycle wildly out of control. Although the government cut two zeroes off the króna in 1981 in order to maintain some sense of normalcy, no substantial policy steps were taken to address the issue.

By the early months of 1983, inflation was pushing 100%. Bjarni Brynjólfsson, editor of the Iceland Review, recalled the era in a 2008 opinion piece:

“I remember getting a weekly pay in cash and the envelope was as thick as a leather wallet. It was a jolly good time. You felt like a king but the many krónas were swiftly washed away as prices kept getting higher. “

Hyperinflation loomed on the horizon and the government was forced to take a number of stabilizing measures: a temporary suspension of wage indexation, a ceiling on wage increases and a compensatory social security and tax exchange to protect individuals. In early 1990, a historic agreement was reached: wage increases would be severely limited nationwide in exchange for the government’s promise to curb inflation. Miraculously, it worked. Inflation dropped to reasonable figures and remained that way until 2008, when the króna and the Icelandic economy went to hell in a hand basket.

“The króna fell like a stone” Ólafur Ísleifsson, assistant professor at Reykjavík University’s business school, recently said. He wasn’t exaggerating: the króna lost half of its value in a matter of days. Inflation reared its ugly head again and topped out at over 18% as Icelanders wearily celebrated the arrival of 2009.

“Ch-ch-ch-changes, Just Gonna Have to be a Different Man”

“The basic economic lesson is that a free-floating currency in the smallest currency area known to man—consisting of 300,000 people—is a recipe for disaster,” Ólafur commented.

“I think that history suggests quite strongly that we would have been better off if we had accepted the offer in 1993 to get into the fast track for EU membership. If we had had the Euro, the economic collapse of 2008 would not have happened.”

Looking ahead, assistant professor Katrín Ólafsdóttir, Ólafur’s colleague at the University, goes one step further: “I don’t think there’s a future for the króna. Absolutely not.

We should do whatever we can to change the currency to the Euro—the sooner, the better… Yes, we would have less economic growth, but we’d also be more stable.”

With a recent poll indicating less than a third of Icelanders wanting to join the EU—much less adopting the Euro—that switch might be easier imagined than realized any time soon. Until then, we might as well indulge in all the zeros in our pockets.

Inflated Crowns

/